Whether we like it or not, money plays a massive role in our daily lives. It is the tool we use to put food on the table, cover our bills, travel to new places, and take care of our families. Yet, many people put off saving money because they think they have all the time in the world.

If you talk to people who have built real wealth, they will all tell you the same thing: time is your greatest asset.

You do not need a massive income to start building a secure future. Even setting aside a small amount of money from every paycheck can completely change your life over time. The earlier you build this habit, the easier it becomes to reach big goals like buying a home, starting a business, or retiring comfortably without financial stress.

This deep-dive guide covers exactly why saving early matters, how it protects your mental health, and easy, practical ways to build a savings habit today.

The Power of Starting Early

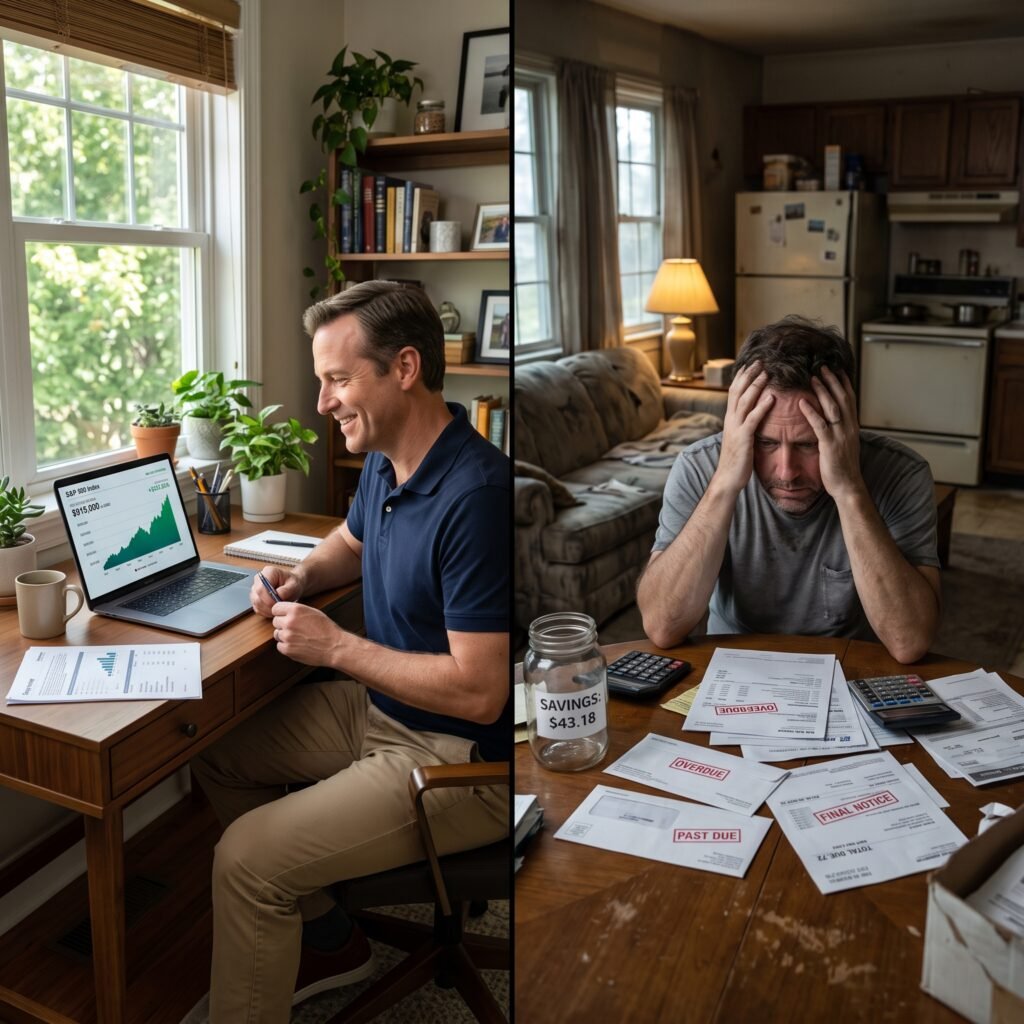

When it comes to money, time is a tool that you can never get back once it is gone. Every single dollar you save in your 20s or 30s has years—or even decades—to sit and grow.

When you delay your savings goals, you lose a massive advantage. Starting early allows small, steady amounts of money to build up into a huge safety net. If you start late, you will have to force yourself to save massive amounts of money each month just to catch up to someone who started early with small change.

1. Compound Growth Works in Your Favor

The absolute biggest mathematical reason to save early is compound growth.

Compound growth means your savings earn interest or returns, and then those returns earn their own returns. It creates a snowball effect. Your money is essentially making new money all by itself, and that new money joins the team to make even more.

A Quick Example of the Snowball Effect

- Person A starts saving $200 a month at age 25.

- Person B waits until they are 40 years old to start saving the exact same $200 a month.

Even though both people are putting away the same amount of cash each month, Person A will end up with vastly more wealth by the time they reach retirement. Why? Because Person A gave their money an extra 15 years to compound and grow.

The earlier you begin, the less heavy lifting your actual pocket has to do, because time does the hard work for you.

2. Financial Emergencies Become Easier to Handle

Life does not care about your plans. It is completely unpredictable. At any moment, you could face:

- An unexpected medical bill

- Sudden car repairs

- An appliance breaking down at home

- Sudden job loss or a drop in work hours

When you do not have any savings, these moments turn into absolute disasters. You are forced to rely on credit cards, expensive personal loans, or borrowing money from friends and family.

Having a dedicated cash cushion changes everything. An emergency fund turns a major life crisis into a minor inconvenience. Building this fund should always be your very first financial milestone.

3. Less Financial Stress and Better Mental Health

Money worries are one of the leading causes of daily stress and anxiety for millions of people. Living paycheck to paycheck means you are always just one bad break away from total ruin. That constant fear takes a heavy toll on your mind, your sleep, and your relationships.

Knowing that you have money set safely aside brings an incredible sense of peace. You do not have to panic when the check engine light comes on in your car. A solid savings account gives you mental clarity, emotional confidence, and total control over your daily life.

4. More Freedom to Achieve Your Life Goals

When you live without savings, you are trapped. You have to stay at a job you hate just to pay next month’s rent.

Saving early buys you your freedom. It gives you options and flexibility to design the life you actually want to live. With a healthy savings account, you can easily say yes to major life goals:

- Buying your first home or apartment

- Stepping away from a 9-to-5 job to start your own business

- Traveling the world and experiencing new cultures

- Going back to school to learn a new skill

- Choosing to retire early to spend time with family

Financial freedom does not start when you become a millionaire. It starts the moment you have enough savings to make your own choices.

5. Avoid the Trap of Unnecessary Debt

People who do not save are target practice for credit card companies and high-interest lenders. When an emergency strikes, borrowing money seems like the only escape route.

However, debt comes with a heavy price tag:

- High-Interest Payments: You end up paying double or triple for items over time.

- Trapped Income: Your future paychecks are already spent before you even earn them.

- Lower Credit Scores: High debt loads make it harder to borrow money at good rates later in life.

By saving early, you become your own bank. When something goes wrong, you pay cash. You completely bypass the debt trap and keep your hard-earned money in your own pocket instead of giving it to a bank.

6. Build Better Daily Financial Habits

Saving money consistently is like going to the gym. It trains your financial muscles and teaches you critical money management skills that stick with you for life.

When saving becomes an automatic part of your monthly routine, you naturally get better at three key things:

Budgeting

You stop wondering where your money went at the end of the month. Instead, you tell your money exactly where to go. Tracking your income and expenses becomes a simple, stress-free habit.

Spending Wisely

You naturally start separating your true needs from your temporary wants. You stop buying things to impress other people and start making smart, intentional purchasing decisions.

Planning Ahead

You break out of the short-term cycle of living week-to-week. You start looking at the bigger picture and making lifestyle choices that protect your long-term future.

7. Reach Retirement Goals Comfortably

Retirement might feel like it is a lifetime away, but time moves incredibly fast. The sooner you start planning for it, the less painful it will be for your wallet.

If you start saving in your 20s, you only need to put away a small percentage of your paycheck to build a massive nest egg. If you wait until your 40s or 50s, you will have to sacrifice a huge chunk of your take-home pay just to build a basic fund. Saving early lets you build wealth gradually, comfortably, and without breaking a sweat.

8. Small Amounts of Money Make a Massive Difference

One of the most common myths is that you need to be rich to start saving. This lie keeps millions of people broke.

The truth is that consistency is infinitely more important than the size of your deposit. Look at how small amounts add up over time:

- $10 per week becomes $520 in a year.

- $25 per paycheck becomes $650 a year (assuming bi-weekly pay).

- $50 per month becomes $600 a year.

Over 5 to 10 years, these small habits turn into thousands of dollars. Never skip saving just because you only have a few dollars to spare. Start exactly where you are with whatever you have.

9. Understanding the Truth About Income vs. Time

A vital lesson about wealth is that you cannot get truly rich by simply trading your time for money.

Think about professionals like doctors or lawyers. They can charge hundreds of dollars per hour, but their income is still completely capped by the number of hours they can work in a day. If they stop working due to illness or exhaustion, their income drops to zero instantly.

To build real security, you must use your early savings to buy assets that separate your income from your time. This means putting money into things that pay you even when you are asleep, such as:

- High-yield savings accounts that pay steady interest

- Dividend-paying stocks

- Real estate or rental properties

- A business or automated side hustle

Your saved dollars are like little workers. The earlier you collect them, the sooner you can set them to work earning passive income for you.

10. Focus on Increasing Income Over Cutting Pennies

While cutting back on small expenses is a great way for beginners to start, frugality has a strict limit. You can only cut your expenses down to a certain point before your quality of life suffers. If someone makes $25,000 a year, skipping their daily cup of coffee is not going to make them rich.

The real path to financial independence is a two-step process:

- Keep your expenses stable and reasonable.

- Focus your energy on growing your income.

Instead of spending hours obsessing over saving a couple of bucks, use that time to upgrade your skills, get a promotion, find a higher-paying job, or start a side business. When your income grows, keep your lifestyle the same and funnel that extra cash directly into your savings. That is how real wealth is created.

Practical Tips to Start Saving Money Today

Ready to start building your financial safety net? Here are five practical steps you can take immediately:

- Create a Simple Monthly Budget: Write down exactly how much money comes in and exactly what goes out. Track every single utility, subscription, and grocery bill.

- Pay Yourself First: Do not save what is left over at the end of the month, because usually, nothing is left. Instead, move a set amount of money into your savings account the absolute second you get paid.

- Automate Your Savings: Set up your bank account to automatically move $20, $50, or $100 from your checking account to your savings account every single payday. This takes human laziness out of the equation.

- Audit Your Unnecessary Spending: Take an afternoon to look through your bank statements. Cancel subscription services you do not use, cut back on eating out at expensive restaurants, and stop making impulse purchases online.

- Set Clear, Visible Financial Goals: Saving is boring if you do not have a target. Give your savings accounts names like “Emergency Fund,” “House Down Payment,” or “Summer Vacation.” Having a clear target makes it easy to stay motivated.

The “Buy It Twice” Rule for Smart Spending

As you start saving, you will face the temptation to upgrade your lifestyle. A brilliant rule of thumb used by self-made millionaires is simple: If you cannot buy something twice with cash, you cannot afford it.

This rule is a shield against lifestyle inflation and impulse buying. If you see a luxury watch or a high-end designer bag that costs $500, ask yourself: “Do I have $1,000 sitting in my account that I am willing to part with right now?” If the answer is no, leave it on the shelf. This mindset ensures you never drain your savings for items that lose value the moment you buy them.

The Hidden Truth: Pre-Tax Income vs. After-Tax Money

Every time you buy a non-essential item, you need to understand the true math behind the purchase. Most people look at the price tag on a item and compare it directly to their hourly wage. This is a massive mistake because of taxes.

When you earn money at a traditional job, you are paid in pre-tax dollars. However, every single item you buy at a store is bought with after-tax dollars.

The Real Cost Breakdown

Imagine you make $50,000 a year, and your total tax rate is around 27%. That means for every $100 you earn at work, you only get to keep $73 in your wallet.

If you want to buy a luxury item that costs $500 cash at the store, you actually had to earn roughly $684 at your job to clear enough money to pay for it.

| Item Price (After-Tax) | True Cost in Labor (Pre-Tax Earnings) |

| $50 | ~$68 |

| $100 | ~$137 |

| $500 | ~$684 |

| $1,000 | ~$1,369 |

When you realize how much real labor and tax effort goes into every dollar you spend, saving that money becomes a lot more attractive than wasting it on temporary items.

Common Savings Mistakes to Avoid

To ensure your savings strategy actually works long-term, stay far away from these common mental traps:

- Waiting for the Perfect Time: There is no perfect time. If you wait until you get a raise, get married, or move houses, you will wait forever. Start today with whatever amount you have.

- Saving Only What is Left Over: This is a guaranteed way to save zero dollars. Always pay yourself first.

- Ignoring the Emergency Fund: Do not put all your extra cash into long-term investments or locked accounts before you build a basic 3-to-6 month cash safety net.

- Treating Savings Like a Checking Account: Keep your savings in a separate bank account entirely. If it is too easy to transfer money back to your checking account via a phone app, you will constantly dip into it for casual spending.

- Setting Unrealistic Goals: Do not try to go from saving zero dollars to saving 50% of your paycheck overnight. You will burn out and quit. Start small, build the habit, and scale up naturally.

Key Takeaways

- Time Beats Everything: Starting early gives your cash the maximum amount of time to grow via compound growth.

- Safety Net First: Savings shield your mental and financial life during sudden emergencies.

- Stress Reduction: A healthy cash cushion lowers daily anxiety and protects your mental well-being.

- Freedom and Flexibility: Savings give you the power to change jobs, start businesses, and make bold life choices.

- Consistency Wins: Small, steady deposits matter infinitely more than waiting to make a single large deposit.

- Earn with Assets: Use savings to buy things that earn money independently from your time.

- Watch the Real Cost: Remember that everything you buy uses after-tax money, which costs more hours of work than the price tag shows.

Frequently Asked Questions (FAQ)

Why is it so much better to start saving early rather than later?

Starting early activates the power of compound growth. Your money has more time to earn returns, meaning your cash does the hard work of building wealth for you over decades. It also helps you build healthy financial habits when life is less complex.

How much money should a absolute beginner save each month?

A standard benchmark is to try to save 10% to 20% of your total take-home income. However, if your budget is incredibly tight, do not stress. Start by saving just $5 or $10 a week. The goal is to build the consistent habit first, then increase the amount later.

What should be my very first savings goal?

Your absolute first priority should be building an emergency fund. Try to save up enough cash to cover $1,000 for immediate emergencies, and then grow that fund until it can cover 3 to 6 months of your basic living expenses (like rent, food, and bills).

Is it too late for me to start saving if I missed my 20s?

Absolutely not. While starting early is ideal, the absolute best time to start saving is always today. Every dollar you save right now will protect your future self.

Should I focus on saving cash or paying off my debts first?

It is usually best to do both at the same time. First, build a small starter emergency fund of about $1,000 so you do not have to take on new debt if something breaks down. Once you have that safety net, throw all your extra cash toward wiping out high-interest debts (like credit cards) while keeping up your basic savings habit.

What is the easiest way to stop dipping into my savings account?

The best trick is to open your savings account at a completely separate bank from your daily checking account. Do not connect a debit card to it, and do not download the app on your phone. Make it a slow, deliberate process to move money out so you are never tempted to use it for impulse purchases.

Conclusion

Deciding to start saving early is one of the most important, life-changing choices you will ever make. It is not about depriving yourself of fun today; it is about respecting your future self. It provides a shield against life’s unexpected disasters, lowers your daily stress levels, and opens the door to genuine financial freedom.

You do not need a massive corporate income or a finance degree to start. What matters most is building the unstoppable habit of consistency. Small, quiet actions taken today turn into massive opportunities down the road.

The absolute best time to start saving was years ago. The second-best time is right now. Open your account, automate a small transfer, and let time do the rest.