Do you feel like your money vanishes every single month? Do you look at your bank account and wonder where all your hard-earned cash went? You are not alone. Millions of people struggle with this exact same problem. In fact, not knowing where your money goes is the number one reason why budgets fail.

The good news is that keeping track of your money does not have to be hard, stressful, or full of boring math. You do not need to be a financial expert to build good habits.

This guide will teach you the easiest, most practical ways to track your daily spending. By using these simple steps, you can take complete control of your cash, stop stressing about bills, and start growing your savings consistently.

Why Tracking Your Expenses Matters

Before we look at how to track your money, we need to understand why it is so important. Think of tracking your spending like looking at a map before a road trip. If you do not know where you are starting from, you cannot find the right way to your destination.

Without tracking your spending, making a budget is just guessing. When you write down every dollar or pound you spend, you gain real financial power.

Here is exactly what happens when you start tracking your money regularly:

- You see the truth: You learn exactly where your money goes instead of guessing at the end of the month.

- You find hidden leaks: You instantly spot tiny, unnecessary costs that are draining your bank account.

- You stop overspending: It creates a natural speed bump in your mind before you buy things you do not really need.

- You save effortlessly: Good saving habits become automatic because you know exactly how much cash is left over.

- You gain peace of mind: You feel calm and confident because you are the boss of your money.

READ MORE

Step 1: Choose Your Tracking Method

There is no single “right” way to track your money. The best method is simply the one that you can stick with every week. People live different lifestyles, so choose one of these three easy systems that fits your daily routine best.

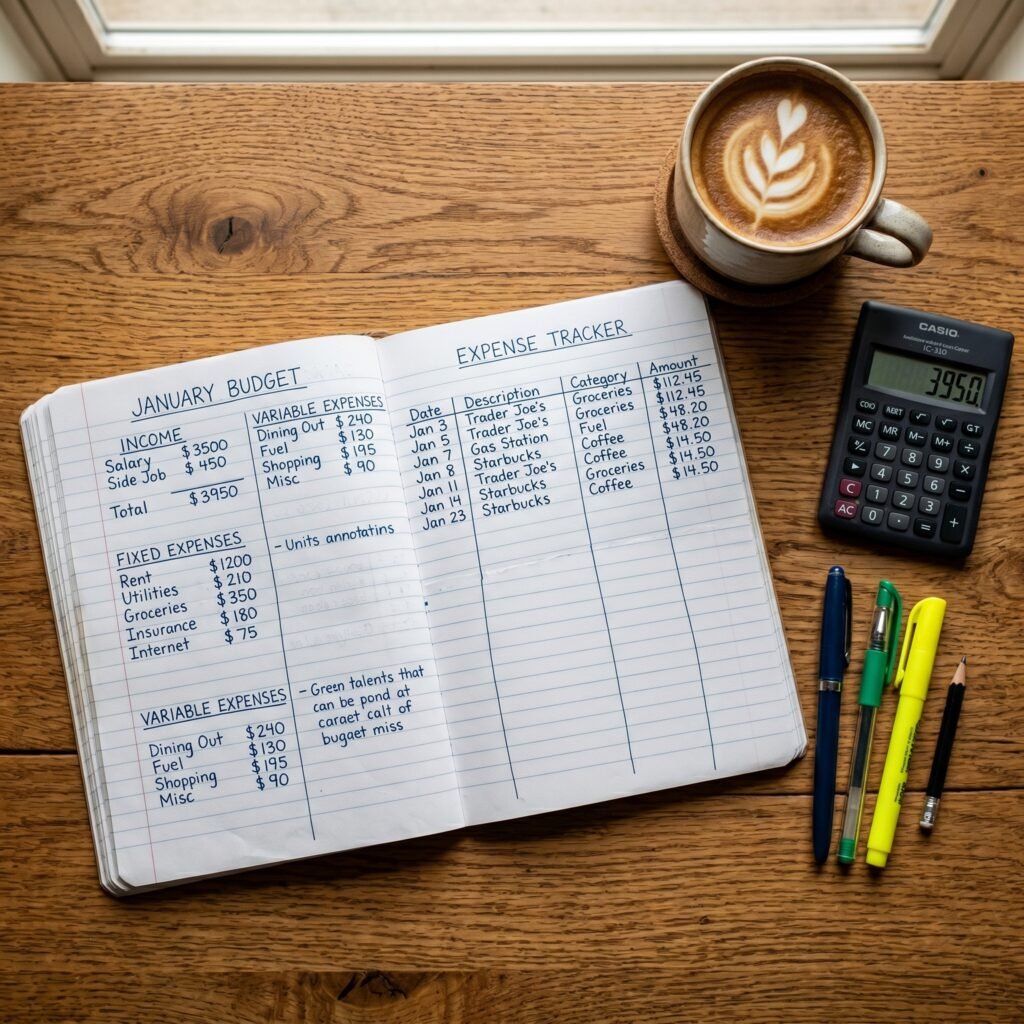

1. The Pen and Notebook Method

This is the most classic and simple way to track money. All you need is a small notebook and a pen. Every time you buy something, you simply write down the item and the cost.

- Who it is for: People who love putting pen to paper and want to stay completely offline.

- Why it works: Writing things down by hand forces your brain to slow down and physically acknowledge the money leaving your pocket. Many successful people use a simple notebook once a year or once a month to clear their heads and look at their habits clearly.

2. The Spreadsheet Method

This method uses free computer tools like Google Sheets or Microsoft Excel to record your income and costs. You can create columns for the date, the store name, the amount spent, and the category.

- Who it is for: People who love clean organization and want full control over their data without paying for fancy tools.

- Why it works: Spreadsheets can do the math for you automatically. By using simple formulas like

SUM, you can add up hundreds of rows of spending in a single second. It gives you a perfect visual view of your entire financial life on one screen.

3. The Expense Tracking Apps Method

If you want technology to do the hard work for you, budgeting apps are a fantastic choice. Tools like YNAB (You Need A Budget), PocketGuard, or similar local bank tracking apps can connect securely to your bank accounts.

- Who it is for: Busy people who want their spending sorted out automatically.

- Why it works: These apps automatically download your bank transactions and put them into neat categories. This minimizes the manual work you have to do, making it much easier to stay consistent over the long term.

Step 2: Categorize Your Expenses (The Needs vs. Wants Rule)

If you just look at a long list of numbers, your brain will get tired. To make tracking easy, you must sort your spending into clear, simple boxes.

A great way to start is by dividing your financial life into three major areas. This is often called the 50/30/20 Rule, which is a highly trusted framework used by financial advisors:

- Needs (Around 50% of your income): These are the essential costs you must pay to survive. This includes rent or mortgage payments, electricity, water, basic groceries, insurance, and necessary transportation.

- Wants (Around 30% of your income): These are things that make life fun but are not required for survival. This includes dining out at restaurants, movie subscriptions like Netflix, shopping for new clothes, hobbies, and holidays.

- Future Savings & Debt (Around 20% of your income): This is the money you put away for your future self. It includes retirement funds, emergency savings pots, stock market investments, or extra payments to clear off student loans and credit cards.

To make your daily tracking clear, use these specific standard categories inside your notebook or spreadsheet:

- Housing: Rent, mortgage, or home fees.

- Utilities: Electricity, gas, water, internet, and mobile phone bills.

- Groceries: Basic food items from the local supermarket.

- Transportation: Fuel for your car, public transit tickets, or car repairs.

- Entertainment: Eating out, ordering takeout food, drinks with friends, and movie tickets.

- Subscriptions: Monthly apps, gym memberships, and streaming services.

- Savings: Money moved directly into investment accounts or emergency funds.

Step 3: How to Build the Spreadsheet System (Step-by-Step)

If you choose to use the spreadsheet method, you need to know how to set it up correctly so it doesn’t become a messy pile of numbers. Real financial clarity comes from cleaning up your data.

Here is the exact step-by-step process to build a professional, clean expense tracker from scratch:

Step A: Download Your Bank Data

Do not waste hours typing out every single transaction from memory. Log into your online banking app via a computer. Look for a button that says “Export as CSV” or “Download Spreadsheet.”

A CSV file is a simple text file that opens instantly in Excel or Google Sheets. If you have multiple bank accounts—such as a salary account, a daily spending account, and a joint account for family expenses—download the data for the past month from all of them.

Step B: Combine and Format the Rows

Copy and paste all your bank data into one main master sheet. Clean up the columns so they look identical.

Important Data Clean-Up Tip: Different banks format spending differently. Some banks show money you spent as a negative number (like -$10), while others show it as a positive number in a “debits” column. Make sure all the money you spent is formatted the same way—preferably as simple numbers—so your formulas do not get confused.

Step C: Delete the Noise

To save time, filter out transactions that are tiny or irrelevant. For example, you can safely delete or ignore rows under $1 or £1, as they will not change your final big-picture numbers. Focus your energy on the real spending.

Step D: Use the “SUMIF” Formula to Automate Your Totals

Once you assign a category word (like “Groceries” or “Entertainment”) next to each transaction row, you can use a powerful spreadsheet formula to add up the totals instantly.

Instead of adding rows manually, type this formula into your summary box:

=SUMIF(Category_Column, "Groceries", Amount_Column)

This formula tells the computer: “Look through my entire list of spending, find every row marked ‘Groceries’, and add those numbers together instantly.” Repeat this simple formula for each of your categories.

Step E: Sort from Largest to Smallest

Once your totals are ready, sort your category list from the highest cost to the lowest cost. This instantly shows you your biggest financial leak. It takes away the guesswork and tells you exactly where your focus needs to be.

Step 4: Record Every Expense Daily

Consistency is the secret sauce of financial freedom. The biggest trap people fall into is waiting until the end of the month to record their spending. By then, receipts are lost, small cash purchases are forgotten, and the task feels too big to handle.

Make it an unshakeable habit to record your expenses every single day. It takes less than two minutes if you do it consistently.

- Tie it to a daily habit: Do it while drinking your morning coffee, or right before you brush your teeth at night.

- Every dollar matters: That small $2 morning coffee or a quick $3 smartphone app purchase might seem harmless. But if you do it every working day, that is over $100 a month flying out of your pocket unnoticed.

- Keep receipts: If you use cash, snap a quick photo of the receipt on your phone so you don’t lose the memory of it.

Step 5: Review Your Spending Weekly

Tracking your money is useless if you never look at the data. Set a recurring appointment with yourself every single week. Sunday evening is the perfect time for most people because life slows down and the working week is ahead.

Sit down in a comfortable chair, put on a relaxing music playlist, and open your tracker. This should be a positive experience, not a punishment.

During your weekly review, ask yourself these three critical questions:

- Did I overspend in any specific area this week? If your entertainment budget is gone by Thursday, you know you need to stay home over the weekend.

- Which category is draining the most cash? Is your food delivery cost shockingly high? Knowing this allows you to adjust immediately before the month ends.

- What can I realistically cut back on next week? Find one small victory you can achieve in the upcoming seven days.

Step 6: Set Realistic Spending Limits

Once you have tracked your money for at least two to three weeks, you will clearly see your natural spending patterns. Now it is time to set clear boundaries.

Do not make your limits incredibly strict right away. If you currently spend $600 a month on dining out, setting a limit of $50 next month will only cause frustration, and you will likely give up. Instead, lower your limits step by step.

Create a simple monthly limit plan like this:

- Groceries Limit: $350 / month

- Entertainment Limit: $150 / month

- Shopping Limit: $100 / month

- Subscriptions Limit: $50 / month

If you see that you are approaching your limit early in the month, look for free alternatives. Instead of going to an expensive restaurant, invite friends over for a home-cooked dinner.

Step 7: Automate Your System to Save Time

The less manual work you have to do, the more likely you are to keep tracking your money for years to come. Automation helps eliminate human error and laziness.

Here are the best ways to put your money tracking on autopilot:

- Set up bank alerts: Turn on instant push notifications inside your mobile banking app. Every time your card is swiped, your phone will instantly pop up with the exact amount spent. This keeps spending at the front of your mind.

- Automate your savings entries: If you have a set amount of money moved into your retirement or stock market accounts on the first day of the month, write it into your tracker as a recurring fixed cost.

- Clean up your subscriptions: Use your tracking review to find sneaky recurring bills. It is incredibly common to find a $15 monthly video streaming pass, an old gym membership, or a software trial that you forgot to cancel. Cancel them immediately to save hundreds of dollars automatically.

Step 8: How to Optimize Your Real Income

Tracking your spending is only one side of the financial coin. The other side is the money coming in. Once you have mastered your costs, look closely at your income column.

If you want to build wealth quickly, you cannot just rely on cutting back on coffee. You also need to look for ways to expand your income safely and intelligently.

1. The Power of Salary Negotiation

If you have been working at your current job for a year or more, it is highly recommended to speak with professional job recruiters in your industry. Find out what other companies are paying for your exact same role.

Even if you love your current boss and have zero interest in leaving, knowing your market value gives you immense leverage. You can confidently schedule a meetings with your employer, showcase the great work you have done over the past year, and negotiate a higher salary based on real industry data.

2. Deploy Your Cash Effectively

Do not let your extra cash sit idle in a basic checking account earning zero interest. Inflation will slowly eat away at its value. Instead, put your money to work:

- High-Yield Savings Accounts: Move your emergency cash into a savings account that offers a competitive interest rate. This keeps your cash safe and accessible while earning passive money every month.

- Automated Investing: Use trusted, low-cost investing platforms to automate your long-term wealth building. Many modern apps allow you to set up automatic deposits directly from your bank account every single month. They can instantly distribute your funds into safe, global index funds (like the S&P 500) based on your personal preferences. This ensures your future wealth grows consistently without you having to trade stocks manually every day.

Step 9: Track and Calculate Your Net Worth

Once you feel comfortable tracking your daily spending and income, it is time to look at the ultimate scoreboard of your financial health: Your Net Worth.

Tracking your net worth is something you should do every three to six months. It helps you see the big picture and ensures you are moving in the right direction over the years.

Calculating your net worth is incredibly simple. It uses a very basic equation:

$$\text{Assets} – \text{Liabilities} = \text{Net Worth}$$

What are Assets?

Assets are things you own that have real cash value. Examples include:

- The money inside your checking and savings accounts.

- The current value of your retirement funds and stock market portfolios.

- The market value of physical property you own (like a house or car).

What are Liabilities?

Liabilities are financial debts that you owe to someone else. Examples include:

- The remaining balance on your home mortgage.

- Student loan balances.

- Credit card debt or personal bank loans.

Grab a dedicated notebook or open a clean spreadsheet tab. List out all your assets on one side, list all your liabilities on the other side, and subtract the total debt from your total assets.

Do not worry if your starting number is small or even negative due to student loans. The exact number does not matter today. What matters is the direction of travel. As you track your expenses daily, cut out waste, and invest consistently, you will watch your net worth line climb higher and higher over the next 3, 5, and 10 years.

Real Life Case Study: Switching to Save

To understand how tracking changes everything, look at how small adjustments create massive wealth over time.

A young professional living in a major city noticed during a monthly expense tracking review that their monthly grocery bill at a premium supermarket chain was completely out of control. They decided to make a deliberate switch to a discount supermarket chain (like Aldi) for their weekly food shopping.

By making this single, simple adjustment, they saved roughly $200 every single month without changing the quality or amount of food they ate.

Instead of spending that saved money on random shopping, they set up an automated transfer to move that $200 directly into a low-cost stock market index fund every month. Assuming a standard annual stock market return, that single change of switching supermarkets can grow into over $30,000 in wealth over a ten-year period. That is the real power of tracking your expenses and taking action.

Key Takeaways for Quick Scanning

If you are in a rush, here are the core lessons you need to remember to take control of your money today:

- Budgeting is guessing without tracking: You must know your past spending numbers to build a successful financial future.

- Pick a system you love: Whether you prefer a physical paper notebook, an Excel spreadsheet, or a fully automated smartphone app, choose the system that feels easiest for you.

- Group your costs simply: Use the 50/30/20 framework to divide your cash into Needs, Wants, and Future Savings.

- Review your data weekly: Set a fixed calendar reminder every Sunday evening to check your tracker and catch overspending early.

- Optimize both sides of the coin: Track your expenses to stop money leaks, but also look for active ways to grow your income and automate your investments.

- Focus on consistency, not perfection: Missing one day of tracking will not ruin your finances. Just pick your tracker back up the next day and keep moving forward.

Frequently Asked Questions (FAQ)

1. What is the single easiest way for a beginner to track expenses?

The easiest way for a beginner is to use a dedicated budgeting app that connects directly to your bank account. It removes the need to write down every single transaction manually, sorting your purchases into neat categories automatically while you sleep.

2. Do I really need to track tiny purchases like a $2 coffee?

Yes, absolutely. Small daily purchases seem completely harmless at the moment, but they add up to huge sums over weeks and months. Tracking small purchases creates true mental awareness of where your cash is going.

3. How often should I check my expense tracker?

You should record your spending daily so you do not forget any transactions. However, you should do a deep review of your total numbers once a week to see if you are staying within your chosen category limits.

4. Is Google Sheets or Excel safe and effective for money tracking?

Yes, spreadsheets are one of the most effective and safe tools available. Because you do not have to link your live bank passwords to a third-party app, it provides incredible privacy while allowing you to build completely customized formulas.

5. What should I do if my net worth calculation is currently negative?

Do not panic. A negative net worth is incredibly common for young professionals who have recently graduated with student loans or bought their first home. The purpose of tracking your net worth is simply to ensure that your debts are going down and your savings are going up every single year.

Conclusion

Tracking your expenses is not about restricting your freedom or stopping you from enjoying life. It is the exact opposite. It is about understanding the flow of your money so you can spend it intentionally on things that truly matter to you.

When you know exactly where your money goes, you stop feeling anxious when paying bills. You gain the clarity needed to make smart, confident financial decisions that protect your future.

Start small today. Pick one tracking method, download your past bank data, and look at the numbers clearly. Stay consistent for just a few weeks, and you will see a massive, positive transformation in your financial health and peace of mind.