Your credit score is the most important number in your financial life. You will never see it on a job offer or a housing application, but it follows you everywhere. It decides whether you get an apartment, a car loan, or a premier credit card—and exactly how much it will cost you.

When your credit score jumps by 50 to 100 points, your entire life instantly becomes cheaper. The interest rates drop, required deposits disappear, and banks start competing for your business instead of denying your applications.

This guide breaks down everything you need to know about navigating the US credit system in 2026. You will learn the best starter cards to build your history, how the credit scoring system calculates your number, and proven steps to raise your score quickly.

The Best Credit Cards for Beginners in USA

If you are starting your credit journey from scratch, your first move is to open a beginner-friendly credit card. You do not need to open a dozen cards. For a beginner, opening just one or two cards is the perfect way to build a solid foundation.

When evaluating a starter card, you need to look at five critical factors:

- Sign-up Bonus: The welcome reward the bank gives you for spending a specific amount of money early on.

- Earnings Rates: The cash back or points you earn on daily purchases like gas, groceries, and dining.

- Benefits: Extra perks like purchase protection, streaming credits, or access to travel ecosystems.

- Annual Fee: The yearly cost to keep the card open (ideally $0 for beginners).

- The Verdict: The final recommendation on who this card is best for.

Here are the six best beginner credit cards available in the USA for 2026.

1. Chase Freedom Unlimited®

The Chase Freedom Unlimited is one of the most powerful starter cards because it introduces you to a massive rewards ecosystem.

+---------------------+---------------------------------------------------------+

| CARD FEATURE | DETAILS & RATES |

+---------------------+---------------------------------------------------------+

| Sign-up Bonus | $250 cash back after spending $500 in the first 3 months|

| Introductory APR | 0% promotional APR for the first 15 months |

| Annual Fee | $0 |

+---------------------+---------------------------------------------------------+

Earning Structure

- 5% cash back on travel booked directly through the Chase Travel Portal.

- 3% cash back on dining purchases (including takeout and eligible delivery services).

- 3% cash back at drugstores.

- 1.5% cash back on all other everyday purchases.

READ MORE

Key Benefits

This card comes with valuable partner perks, including an extra 5% cash back on Lyft rides and 3 months of complimentary DoorDash DashPass access.

However, the greatest unpublished benefit is that it gets your foot in the door with Chase. Building a strong banking relationship with Chase early makes it much easier to get approved for higher-tier cards later, such as the Chase Sapphire Preferred® or Chase Sapphire Reserve®.

The Verdict & Recommendation

The Chase Freedom Unlimited is an exceptional first card. It lets you dip your toes into the credit world with no annual fee while earning highly competitive cash back on dining and daily spending.

2. Discover it® Cash Back

The Discover it® card is famous for being highly accessible to beginners while offering an incredibly lucrative first-year promotion.

+---------------------+---------------------------------------------------------+

| CARD FEATURE | DETAILS & RATES |

+---------------------+---------------------------------------------------------+

| Sign-up Bonus | Unlimited Cashback Match (Matches all year-1 rewards) |

| Introductory APR | 0% promotional APR for the first 15 months |

| Annual Fee | $0 |

+---------------------+---------------------------------------------------------+

Earning Structure

- 5% cash back on rotating categories each quarter (up to $1,500 spent per quarter, activation required).

- 1% cash back on all other purchases once you hit the quarterly limit.

Note: In 2026, these quarterly categories typically include everyday essentials like gas stations, grocery stores, Amazon.com, and online shopping.

Key Benefits

The standout feature is the Unlimited Cashback Match. Discover automatically matches all the cash back you earn at the end of your first year. This means your 5% categories effectively become 10% cash back, and your everyday 1% spending becomes 2% cash back. The card also charges absolute zero foreign transaction fees, making it safe to use when traveling outside the US.

The Verdict & Recommendation

Discover is widely known for its excellent customer service and high approval rates for thin credit files. If your primary goal is maximizing pure cash back in your first 12 months while learning how rotating categories work, this card is an absolute no-brainer.

3. Citi Double Cash® Card

If you do not want to track rotating categories or manage complicated travel portals, the Citi Double Cash keeps your finances incredibly simple.

+---------------------+---------------------------------------------------------+

| CARD FEATURE | DETAILS & RATES |

+---------------------+---------------------------------------------------------+

| Sign-up Bonus | $200 cash back after spending $1,500 in the first 6 mos |

| Annual Fee | $0 |

+---------------------+---------------------------------------------------------+

Earning Structure

- 2% cash back on everything: You earn an unlimited 1% cash back when you buy an item, and another 1% cash back when you pay it off.

Key Benefits

This card cuts out all the bells, whistles, and confusion. There are no spending caps, no category restrictions, and no complex rules to memorize.

For intermediate users, it serves as a great companion card to pair with the premium Citi Strata Premier℠ card. You can move your Double Cash rewards over to the premium card to unlock high-value airline transfer partners like American Airlines.

The Verdict & Recommendation

This is the ultimate “Keep It Simple” credit card. If you want a reliable, no-nonsense card that guarantees a flat 2% return on every single dollar you spend while you practice paying your bills on time, choose the Citi Double Cash.

4. Bilt Obsidian Card

The Bilt Obsidian is a “Beginner Plus” card designed specifically for renters and young professionals who want to maximize their largest monthly expense.

+---------------------+---------------------------------------------------------+

| CARD FEATURE | DETAILS & RATES |

+---------------------+---------------------------------------------------------+

| Sign-up Bonus | $200 Bilt Cash upon account approval |

| Annual Fee | $95 |

+---------------------+---------------------------------------------------------+

Earning Structure

- 4% cash back (as Bilt Cash) on all purchases, OR choose to earn up to 1.25x points on your rent or mortgage payments.

- 3x points on your choice of either dining or groceries (up to $25,000 per year, then 1x).

- 2x points on travel purchases.

- 1x points on all other spending.

Key Benefits

This is one of the only credit cards in the US financial market that allows you to earn points on rent or mortgage payments with absolutely zero transaction fees. If you pay rent through the Bilt app or an integrated property portal, you turn a massive monthly bill into valuable rewards.

Bilt points are incredibly valuable because they transfer directly at a 1:1 ratio to elite travel partners, including Hyatt Hotels, Alaska Airlines, and Japan Airlines (JAL). For example, a luxury night at the Park Hyatt New York can cost over $1,000 cash, but you can book it for just 35,000 Bilt points.

Additionally, on the first day of every month (“Bilt Rent Day”), you get access to double point earnings, massive airline transfer bonuses (sometimes up to 100%), and elite hotel status matches. The card also includes a $100 annual hotel credit when booking through the Bilt Travel Portal (split as $50 per half-year).

The Verdict & Recommendation

Because this card carries a $95 annual fee and requires a basic understanding of point transfer partners, it is best suited as a second credit card rather than your very first. If you are a renter who wants to turn housing payments into free luxury vacations, this card offers unmatched value.

5. Capital One Savor Rewards Card

The Capital One Savor Rewards card is a highly underrated option that focuses heavily on food, dining, and daily lifestyle categories.

+---------------------+---------------------------------------------------------+

| CARD FEATURE | DETAILS & RATES |

+---------------------+---------------------------------------------------------+

| Sign-up Bonus | $200 cash back after spending $500 in the first 3 months|

| Annual Fee | $0 |

+---------------------+---------------------------------------------------------+

Earning Structure

- 5% cash back on hotels, vacation rentals, and car rentals booked directly through the Capital One Travel Portal.

- 3% cash back on dining (including restaurants, cafes, and fast food).

- 3% cash back at grocery stores (excluding superstores like Walmart and Target).

- 3% cash back on popular streaming services and entertainment options.

- 1% cash back on all other purchases.

Key Benefits

The standout benefit for beginners is that this card has no foreign transaction fees. Most no-annual-fee cards charge a 3% penalty whenever you swipe your card outside the United States. The Capital One Savor avoids this entirely while providing massive 3% returns on the two categories people spend the most money on: food and groceries.

The Verdict & Recommendation

If your monthly budget is heavily dominated by eating out, cooking at home, and streaming entertainment, this card will accumulate cash back faster than almost any other free card on the market.

6. American Express® Blue Cash Preferred®

The Blue Cash Preferred is a premium everyday card that acts as a powerhouse for households with high grocery and commuting expenses.

+---------------------+---------------------------------------------------------+

| CARD FEATURE | DETAILS & RATES |

+---------------------+---------------------------------------------------------+

| Sign-up Bonus | $250 cash back after spending $3,000 in the first 6 mos |

| Introductory APR | 0% promotional APR for the first 12 months |

| Annual Fee | $0 for the first year, then $95 a year after that |

+---------------------+---------------------------------------------------------+

Earning Structure

- 6% cash back at US supermarkets (on up to $6,000 in spending per year, then 1%).

- 6% cash back on select US streaming subscriptions.

- 3% cash back at US gas stations.

- 3% cash back on transit (including trains, taxicabs, rideshares, tolls, and parking).

- 1% cash back on all other purchases.

Key Benefits

The card offers a $120 annual statement credit for Disney streaming services (delivered as $10 per month). If you already pay for Disney+, Hulu, or ESPN+, this credit completely offsets the $95 annual fee, effectively paying you $25 a year to hold the card.

It also includes American Express Return Protection. If you purchase an eligible item within 90 days and the store refuses to take it back, Amex will refund you up to $300 per item (up to $1,000 per calendar year).

The Verdict & Recommendation

An absolute powerhouse for families. If you spend close to $500 a month on groceries, use streaming services, and buy gas frequently, the 6% and 3% return rates make the Blue Cash Preferred one of the most profitable cards you can own.

How Credit Scores Work in Simple Terms

To master your finances, you must understand exactly how the system tracks you. In the United States, your primary credit score is called a FICO Score. This three-digit number ranges from 300 to 850.

Lenders use this score to judge how reliably you manage debt. The system does not care how hard you work, what your job title is, or how much money you have sitting in your checking account. It only looks at your historical tracking data.

Here is exactly what your life looks like at every single tier of the credit score ladder, followed by a breakdown of the math behind the numbers.

The Anatomy of the Credit Score Ladder

The Subprime Floor: 300 to 499

At this level, the financial system penalizes you constantly. If you try to apply for a standard credit card, you are instantly denied. If you apply to rent a $650 apartment, the landlord will either decline your application or require a massive double deposit—forcing you to pay first month, last month, and a heavy security deposit upfront just to get the keys.

If you buy a car from a “Buy Here, Pay Here” lot, you will be hit with a predatory interest rate around 24.9% APR. On a used car, you could easily end up paying over $10,000 in pure interest alone over five years. Cell phone carriers will force you onto expensive prepaid plans because they will not lease you a device. Even your auto insurance premiums will jump automatically simply because your credit file is flagged as high-risk.

The Struggle Tier: 500 to 579

This is the hardest tier because you are actively trying to improve, but the rewards are small. At this level, you can get a “Secured” credit card, which requires you to deposit $200 of your own money to get a matching $200 credit limit. Alternative lenders might offer you a card with a tiny $300 limit, but hit you with a $75 annual fee just for the privilege of opening the account. Car loan interest rates drop slightly to around 18.4% APR, but you are still bleeding thousands of dollars in excess interest.

The Fair Footing: 580 to 619

Here, the walls begin to open slightly. Once you hit 12 to 14 months of consecutive on-time payments, secured cards will “graduate,” meaning the bank refunds your cash deposit and upgrades you to a real, unsecured card. You technically qualify for an FHA Home Loan (which has a 580 minimum threshold). However, the interest rates are steep (often around 7.8%), meaning you will pay hundreds of thousands of dollars extra over a 30-year mortgage compared to top-tier buyers.

The Shifting Math: 620 to 659

At this stage, you begin to experience real financial relief. You can successfully request credit limit increases from your banks. If your credit limit goes from $500 to $1,500 without you increasing your spending, your utilization rate drops automatically, which immediately bumps your score up. You get approved for standard 1.5% cash back rewards cards and car loans drop to around 8.4% APR, saving you thousands compared to the lower tiers.

Approved, But Not Preferred: 660 to 699

At this level, you have a clean file with multiple consecutive on-time payments. You qualify for excellent rotating category cards like the Chase Freedom Flex. You can move away from restrictive government loans and qualify for a conventional home mortgage.

However, you are still one rung below the best pricing. Lenders will approve your applications, but they will charge you a slightly higher “footnote rate” instead of the low rate advertised on their landing page. This small gap can cost you an extra $80 to $100 a month on large loans.

The Safe Zone: 700 to 739

The moment you cross the 700 threshold, money stops leaking from your pocket. Premium pre-approved offers start arriving in your mailbox automatically. Lenders quote you the actual advertised prime interest rates.

When your auto insurance company runs a routine credit check at renewal, your monthly premiums drop without you asking. All major doors—apartments, auto loans, and premier reward cards—open instantly without double deposits or co-signers.

The Preferred Elite: 740 to 799

Banks officially categorize you as a “Preferred” client. You can confidently walk into premium card approvals like the Chase Sapphire Reserve or American Express Platinum. These cards offer luxury airport lounge access, global travel credits, and massive sign-up bonuses that pay you to hold the card.

On a $300,000 home mortgage, a 760 score can easily save you over $180,000 in total interest payments over 30 years compared to someone buying the exact same house with a 540 score. Lenders actively compete for your business, allowing you to choose the best terms.

Financial Sovereignty: 800 to 850

You have achieved an elite status. Your credit report shows zero late payments, very low utilization, and a long history of open accounts. The financial system completely runs out of ways to penalize you. Lenders and mortgage companies will proactively contact you to offer rate reductions and high-value lines of credit. You have total negotiation leverage because banks know you can easily walk away to a competitor.

The 5 Ingredients of Your FICO Score

To move up these tiers, you need to understand the exact mathematical breakdown of your credit score. Your FICO score is calculated using five distinct variables:

FICO SCORE BREAKDOWN

+-----------------------------------------------------+

| [██████████████] 35% Payment History |

| [████████████] 30% Amounts Owed (Utilization) |

| [██████] 15% Length of Credit History |

| [████] 10% New Credit |

| [████] 10% Credit Mix |

+-----------------------------------------------------+

1. Payment History (35%)

This is the single largest component of your score. It measures one basic question: Do you pay your bills on time? A single payment that is 30 days or more late can instantly tank a 750 score down by 100 points. Conversely, maintaining a perfect streak of consecutive, on-time payments is the absolute foundation of building an elite score.

2. Amounts Owed / Credit Utilization (30%)

This measures how much of your available credit limits you are actively using. It is calculated by dividing your total credit balances by your total available credit limits. For example, if you have a card with a $1,000 limit and you carry a $400 balance, your utilization rate is 40%.

To maximize your score, you should always keep your total utilization under 10%. The system views high utilization as a sign of financial stress, even if you pay the bill in full every month.

3. Length of Credit History (15%)

This looks at the age of your financial accounts. Specifically, it averages the age of all your open accounts combined and looks at the age of your absolute oldest account. The longer your accounts have been open and active, the more stable and predictable you look to a bank. This is why you should never close your very first credit card account; closing it shortens your historical timeline.

4. New Credit (10%)

Whenever you apply for a new credit card, auto loan, or mortgage, the lender triggers a “Hard Inquiry” to check your file. Each hard inquiry temporarily lowers your score by a few points and stays on your credit report for up to two years. Applying for multiple credit lines within a short window makes you look desperate for cash, which flags you as a risky borrower.

5. Credit Mix (10%)

Lenders want to see that you can responsibly manage different types of debt simultaneously. Your credit score receives a small boost if you maintain a healthy mix of revolving credit (such as credit cards with variable monthly balances) and installment credit (such as auto loans, student loans, or home mortgages that have fixed monthly payments).

How to Improve Your Credit Score Fast

If your credit score is currently low, or if you want to push it into the elite 750+ range before applying for a major loan, there are proven tactical steps you can take to accelerate the process.

The Method

1.Get Added as an Authorized User:Takes 7-10 Days.

Find a trusted family member or spouse who owns a credit card with an immaculate, long-term payment history and a very low utilization rate. Have them call their bank and add your name as an Authorized User. The bank will report that card’s entire pristine history onto your personal credit profile, instantly injecting years of good history and thousands in available credit into your file.

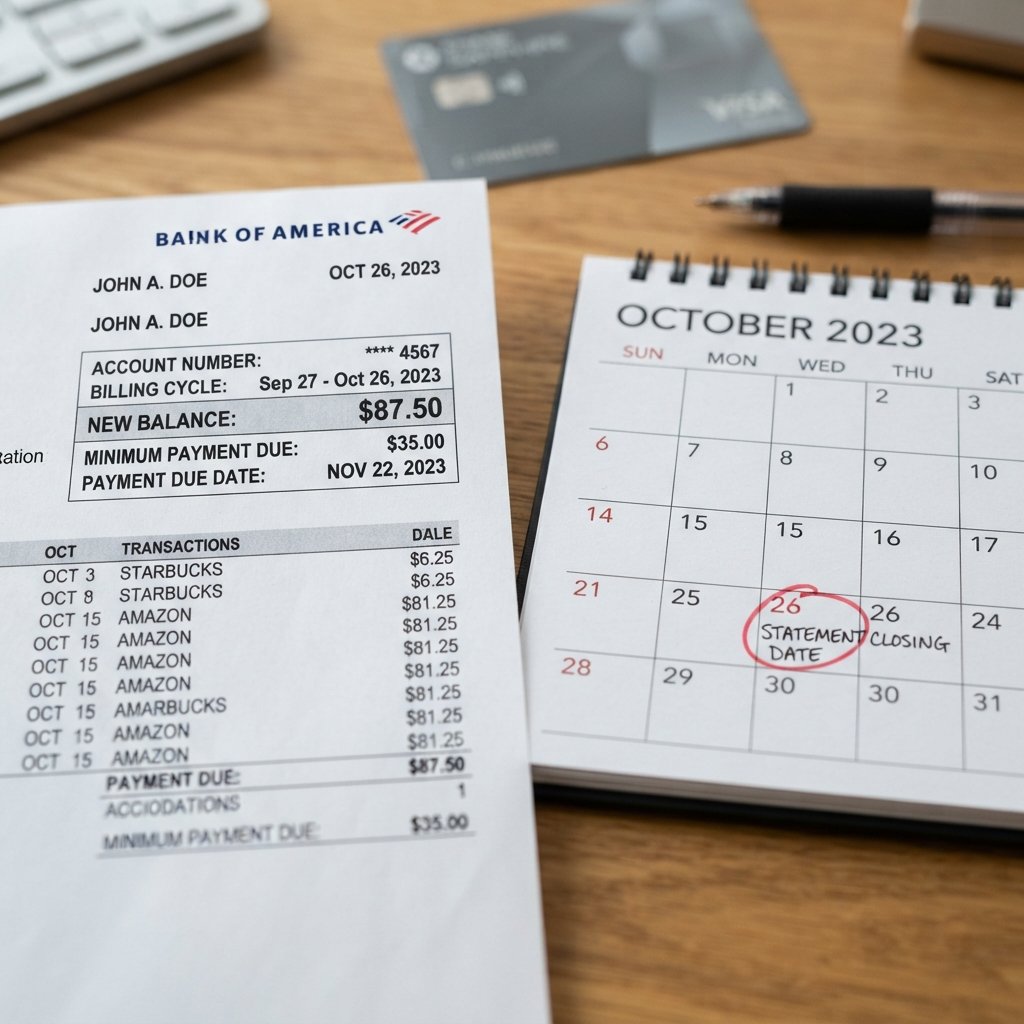

2.Crush Your Credit Utilization Rate:Takes 30 Days.

Log into your accounts and locate your Statement Closing Dates (note: this is completely different from your payment Due Date). Pay your balances down to less than 10% before the statement closing date arrives. Banks report your balance to the credit bureaus on the closing date; by paying early, the system registers a tiny utilization rate, which triggers a rapid score jump.

3.Request Credit Limit Increases:Takes 5 Minutes.

Call your current credit card issuers or use their mobile apps to request a Credit Limit Increase. Ask them explicitly to process the request without running a hard inquiry (a “soft pull” increase). If your limit is increased from $1,000 to $3,000, your daily spending automatically represents a much lower percentage of your overall limit, permanently lowering your utilization.

4.Audit and Dispute Credit Report Errors:Takes 30-45 Days.

Go to AnnualCreditReport.com and pull your official files from Experian, Equifax, and TransUnion. Audit every line item for errors, inaccurate late payments, duplicate collections, or old negative accounts that should have dropped off after 7 years. File an online dispute with the bureaus for any inaccuracies; by law, if a lender cannot verify the error within 30 days, it must be deleted completely.

The 500-to-Prime Credit Repair Strategy

The Method

1.Pull and Audit Your Official Credit Reports:Takes 1-2 Weeks.

Go to AnnualCreditReport.com and pull your three official credit reports (Experian, Equifax, and TransUnion). Do not rely on third-party tracking apps, as they often miss specific details. Highlight every single collection entry and note three vital pieces of data: the Collection Agency Name, the Balance Owed, and the Date of First Delinquency (DOFD).

2.Send Debt Validation Letters:Takes 30 Days.

Before acknowledging or paying a dime, force the collection agency to prove they actually own the debt and have the legal right to collect it. Send a formal Debt Validation Letter via certified mail with return receipt requested. Under the Fair Debt Collection Practices Act (FDCPA), if the agency cannot provide the original contract or proper verification within 30 days, they must legally delete the collection from your report.

3.Negotiate a ‘Pay for Delete’ Agreement:Takes 1-2 Weeks.

If the debt is verified and valid, contact the collection agency to negotiate. Never pay the full amount. Start by offering 30% to 50% of the balance. Crucially, make the payment conditional upon a Pay for Delete agreement. This means you agree to pay a settled amount, and they agree to completely erase the entire collection account from your credit file. Get this agreement in writing or via an official email before sending any funds.

4.Dispute Leftover Inaccuracies:Takes 30-45 Days.

If an agency refuses a Pay for Delete agreement but you choose to pay anyway, or if old unverified items remain, file a formal dispute directly with the credit bureaus (Experian, Equifax, and TransUnion). Dispute specific technical details rather than the debt itself—look for mismatched dates, incorrect balances, or misspelled names. If the bureau cannot verify the accuracy of the technical data with the creditor within 30 days, the entire account is removed.

5.Add Positive Credit Lines Simultaneously:Ongoing.

While you are cleaning up the bad accounts, you must actively build good history, or your score will stay stagnant. Open a Secured Credit Card (like the Capital One Secured or Discover it® Secured) with a small $200 deposit. Put one tiny recurring subscription on it, set it to auto-pay the statement balance in full every month, and leave it alone. This injects fresh, on-time payment history into your profile.

Three Ground Rules for Dealing with Collections

⚠️ 1. Beware the Statute of Limitations: In most US states, a negative item legally drops off your credit report exactly 7 years from the Date of First Delinquency. If an account is 6 years old, it may be wiser to simply let it age and fall off naturally.

📱 2. Never Give Phone Authorization: When negotiating with collectors, keep everything in writing. Never give them verbal access to your checking account or debit card number. If you reach a settlement, pay using a cashier’s check or a secure portal once you have the physical agreement in hand.

🛑 3. Do Not Acknowledge the Debt Blindly: If a collector calls you about an old debt that is past your state’s legal statue of limitations for lawsuits (typically 3 to 6 years depending on the state), verbally acknowledging that you owe the money can accidentally “reset the clock,” giving them the right to sue you again. Always say, “Send me everything in writing for review.”

How to maximize Travel points for business class travel

Maximizing credit card points for business class travel requires collecting high-value flexible points and transferring them directly to airline loyalty programs rather than using standard cash back or basic travel portals.

The Chase Trifecta is a highly popular multi-card setup designed to extract the absolute most points out of everyday spending by combining cards that cover different categories.

1. How the Setup Works

The strategy relies on pooling cash-back rewards from no-annual-fee cards into a premium travel card, which unlocks the ability to transfer points to airlines at a 1:1 ratio.

The standard trifecta consists of three specific cards:

- The Anchor (Chase Sapphire Preferred® or Sapphire Reserve®): You must hold at least one of these premium cards. They allow you to transfer points to airlines and offer bonus points on travel and dining.

- The Multiplier (Chase Freedom Flex®): A no-annual-fee card that earns 5% back (5x points) on up to $1,500 in combined purchases in rotating quarterly categories (like groceries, gas stations, or Amazon).

- The Catch-All (Chase Freedom Unlimited®): A no-annual-fee card that earns a baseline of 1.5% back (1.5x points) on all non-bonus spending, ensuring you never earn just 1x point on a purchase.

Note: If you qualify for business cards, you can substitute or add the Ink Business Cash® (5x on office supply stores/internet) or Ink Business Preferred® to accelerate your earnings.

2. The Execution Blueprint

To maximize your points for a premium cabin, you must route your spending precisely:

1.Match spending to the right card:Daily routine.

Never use your Sapphire card for everyday retail. Use the Freedom Flex for whatever the current 5x quarterly category is. Use the Sapphire card strictly for dining and travel (2x or 3x). Use the Freedom Unlimited for everything else to secure a minimum 1.5x return.

2.Pool your points:Monthly.

Log into your Chase account and use the “Combine Points” feature. Move the cash-back points earned on your Freedom Flex and Freedom Unlimited over to your Sapphire card’s account. This instantly converts basic cash back into high-value Ultimate Rewards points.

3.Find business class award availability:Before transferring.

Do not transfer points blindly. Search for award seats directly on airline partner websites (e.g., British Airways, Air Canada, United). Look for “Saver” level business class tickets, which offer the lowest points cost.

4.Transfer and book:Instant checkout.

Once you find an open seat, link your airline frequent flyer account to Chase and transfer the required points at a 1:1 ratio. Book the business class seat immediately before the inventory disappears.

3. Top Transfer Partners for Business Class

Booking business class through the Chase Travel portal is rarely a good deal because it ties your points to the cash price of the ticket (e.g., a $4,000 flight would cost roughly 266,000–320,000 points). By transferring to airlines, you can often book the same flight for 60,000 to 80,000 points.

Focus on these high-value strategic partners:

- Air Canada (Aeroplan): Exceptional for booking business class on Star Alliance partners (like Lufthansa, Swiss, or ANA) to Europe or Asia. A one-way business class flight to Europe typically ranges from 60,000 to 70,000 points.

- British Airways (Executive Club): Ideal for booking American Airlines or Qatar Airways Qsuite flights. You can transfer Avios easily between British Airways, Qatar, and Iberia to find the lowest booking fees.

- Virgin Atlantic (Flying Club): Great for booking Delta One flights to Europe or ANA First/Business class to Japan at incredibly low point rates, provided you find partner availability.

- United Airlines (MileagePlus): A straightforward option for domestic premium transcontinental flights or international trips on Star Alliance partners with zero added fuel surcharges.

Pro Tip: Keep an eye out for seasonal transfer bonuses. Chase occasionally offers a 20% to 30% bonus when transferring to specific partners like Virgin Atlantic or British Airways, lowering the point requirements for your luxury flight even further.

Frequently Asked Questions (FAQs)

What is the difference between a statement closing date and a payment due date?

Your payment Due Date is the final deadline to pay your bill to avoid late fees and interest charges. Your Statement Closing Date is the last day of the monthly billing cycle. Whatever your balance is on the closing date is what gets reported to the credit bureaus and determines your credit utilization rate. To optimize your score, always pay your balance down before the closing date.

Does carrying a monthly balance on my credit card help build credit?

No. This is a common financial myth that costs people unnecessary money. You do not need to pay interest to build a great credit score. The system tracks whether you pay on time, not whether you carry a balance. Always pay your statement balance in full every month to build history while completely avoiding interest fees.

How long do negative items like late payments or collections stay on my report?

Most negative financial markers—including late payments, collection accounts, foreclosures, and repos—remain on your credit report for exactly 7 years from the date of the original missed payment. Chapter 7 bankruptcies can stay on your report for up to 10 years. As these items age, their negative impact on your score slowly decreases.

What is a good starter credit limit for a beginner in the USA?

For an absolute beginner with a brand-new credit file, a typical starting limit ranges anywhere from $200 to $1,500. If you open a secured card, your limit will directly match the cash deposit you provide. As you maintain a clean track record of on-time payments for 6 to 12 months, banks will naturally increase this limit.

Will checking my own credit score lower my number?

No. Checking your own credit score through monitoring apps, bank dashboards, or official credit report sites is categorized as a Soft Inquiry. Soft inquiries have absolutely zero impact on your credit score and are completely invisible to lenders. Only hard inquiries triggered by formal applications for new loans or cards will impact your score.

Key Takeaways

- Start Small but Smart: Open a no-annual-fee card like the Chase Freedom Unlimited or Discover it to establish a clean banking relationship and practice basic financial discipline.

- Master the Math: Focus 65% of your energy on the two biggest scoring components: making on-time payments (35%) and keeping your credit utilization under 10% (30%).

- Optimize Leverage: Turn major monthly liabilities into assets. If you are a renter, look into intermediate cards like the Bilt Obsidian to earn high-value travel points on housing payments.

- Speed Up the Process: If you need a fast score increase, leverage the authorized user method or shift your payment schedule to clear your balances prior to the statement closing date.